Cheque Stamps

As I have explained under Section 3 of this book, cheques come under the general heading of negotiable instruments, and are closely related to Bills of Exchange. Indeed, the definition of a cheque contained in Section 73 of the Bills of Exchange Act 1882 is as follows:-

"A cheque is a bill of exchange drawn on a banker payable on demand. Except as otherwise provided in this Part, the provisions of this Act applicable to a bill of exchange payable on demand apply to a cheque."

The basic differences between the two types of instrument are:-

-

1. Cheques have to be drawn on a banker, whereas Bills of Exchange can be drawn on anyone. In practise, however, most bills are drawn on bankers.

-

2. Cheques are payable on demand, in other words they can be presented to the bank for payment at any time, provided they are within the statutory expiration time limits of the banking legislation of the country concerned. Bills usually have a future date for presentation specified.

-

3. In the particular case of Mauritius (and in many other countries) Bills of Exchange created Government revenue, as it was mandatory that ad valorem duty had to be paid on the Bill by affixing revenue stamps. Later on, postage and revenue stamps replaced the earlier items. In the case of cheques, the charge was a basic fixed figure irrespective of the amount of the cheque. Latterly, cheques have not been subject to any form of duty.

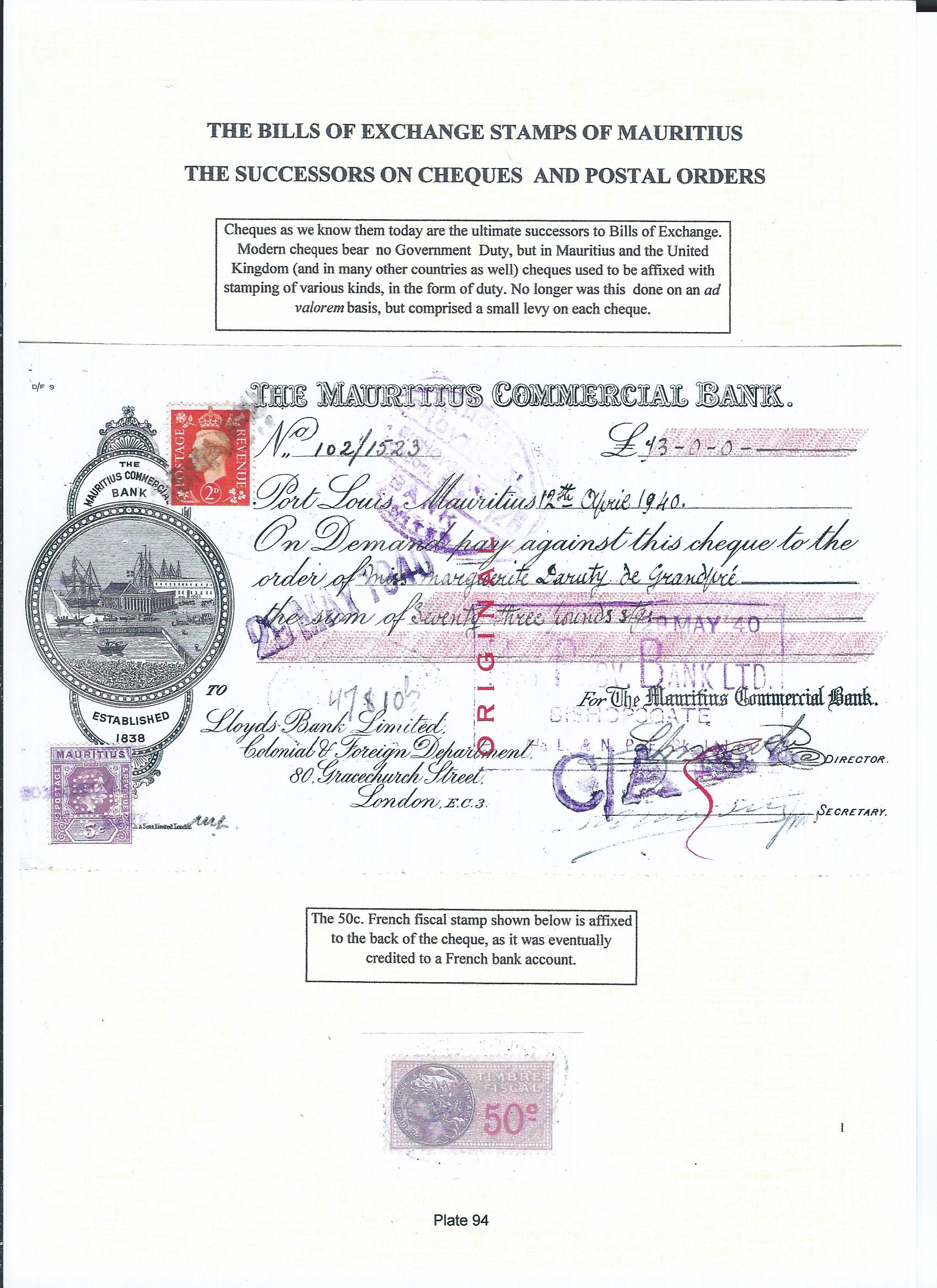

In Plates 94 and 95 there are two examples of rather unusual cheques. They are both drawn by the Mauritius Commercial Bank Ltd in Port Louis, Mauritius, and addressed to Lloyds Bank Ltd, Colonial and Foreign Department at 80 Gracechurch Street, London EC3. The payees are different: Miss Marguerite Daruty de Grandpre and Messrs. W Atlee Burpee. The London bank received both of these for credit of foreign accounts. The cheque on Plate 94 bears, initially on the day of issue 12 April 1949, a King George VI definitive five cents postage and revenue stamp. On reaching London it is affixed with a GB twopenny orange definitive. When it arrives in France it is affixed with a fifty cents stamp on the reverse and credited to the payee's account.

Plate 94 (click to

enlarge)

Plate 95 shows a similar procedure, but in this case

the payee's bank is in Phiadelphia, USA, and there is stamp affixed to

the back of the cheque. I show on

Plate 96 the reverse

copy of this item, not only to illustrate the various endorsements

en route, but to show that the Philadelphian handstamp is complete,

and not partial due to the prior existence of a stamp having been

removed. Not all countries charged duty on cheques, and it may be that

the USA did not. I have not researched this point.

Mauritius archival material is scant indeed in relation to cheques.

Generally speaking stamp duty on cheques has been abolished in recent

years by most, if not all, countries. In Great Britain, according to the

Royal Mail archives, stamp duty on cheques ceased on 1 February 1971,

and it seems likely that Mauritius may have followed suit about the same

time. between the time of using postage and revenue stamps for the duty

levied and the time that duty ceased, most Commonwealth countries

developed a system of oval embossed duty stamps which were impressed on

the face of each instrument. Latterly, this was replaced in about 1956

by a round, double circle printed "stamp duty paid" mark, usually black

in colour circling in the case of Britain and the Commonwealth the Royal

crown.

With the rapid advent of online financial activity, and the

ever-increasing use of credit cards, it is likely that some countries

will seek to abolish the use of cheques in the foreseeable future. Some

are already giving it thought. Rather like thinking in terms of a

cashless society, it will mean some considerable changes, and difficult

in some regions of the world. In Mauritius, cheques represent currently

some 20 per cent of all non-cash transactions. Up until very recently,

all cheques on the island were cleared manually at the clearing house in

Port Louis: this involved manual exchange of about 20,000 cheques each

day. Computer development has enabled a more sophisticated system to be

introduced, known as the Cheque Truncation System (CTS), full details of

which can be found on the internet. Manual presentation of cheques is no

longer necessary, and this enables clearance to take place in one or two

days rather than up to five days before.